Texas Ground-Up Deals We’ve Funded

Here are two Texas ground-up projects we financed from the dirt up — one a first-time investor’s single build, one a sixteen-home development. Real deals, real numbers.

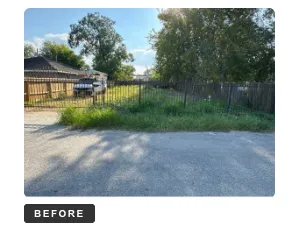

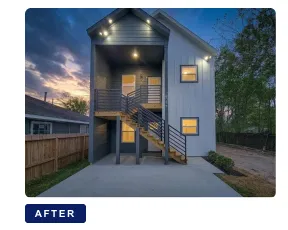

First-Time Investor, Ground-Up Duplex in Houston — Sold for $470,000

This borrower had never owned real estate — no rental, not even a primary home. On paper, most construction lenders stop reading right there. We didn’t, and the reason is the same thing we tell every new builder: in ground-up construction, the number-one risk isn’t your résumé, it’s your builder. This investor had partnered with Grace Building Company, a Houston team we already knew and trusted. Once we vetted the builder and the budget, the rest of the deal got a lot clearer.

Duplex · 2,114 sq ft · each unit 3 bed / 2 bath · Houston, TX 77021

He bought the lot for $95,000 and built a 2,114-square-foot duplex — two units, each 3 bed / 2 bath — in Houston’s 77021. Construction ran $244,620, putting his total cost basis at $339,620. We funded $288,371, roughly 85% loan-to-cost, on our non-dutch draw structure, so he paid interest only on what he’d actually drawn as each phase closed out. The finished duplex sold for $470,000.

The lesson we’d pass to any first-timer: don’t fixate on the builder’s quote alone — watch the timeline. Every extra month of construction compounds your holding costs and eats into profit, so your team’s speed and quality matter as much as the numbers on paper. He got deal #1 right, and we’re now reviewing a four-unit build together.

One $400K Lot, Sixteen New Homes — a Houston Development That Sold for $5.3M

Not every ground-up deal is a single house. This one started as one $400,000 lot in the thick of the Covid market and became a sixteen-home community in southeast Houston.

16 single-family homes · southeast Houston

Our client, Kevan Shelton of Park Street Homes, is a seasoned builder — and he played it patiently. Rather than rushing dirt, he held the land while the market matured, working through the soft costs, engineering, and replatting needed to subdivide a single lot into sixteen individual parcels. Then he built: sixteen well-made single-family homes on ground that used to be one lot.

The project hit every headwind the era had — rising construction costs, crews out sick, and a stretch when plenty of lenders simply paused. We didn’t. We kept the capital flowing on an 18-month construction loan so the build never stalled. By the finish, the sixteen homes appraised at $5.1 million and sold for $5.3 million — on a project that began as a single $400,000 lot. It’s the kind of deal that only works when the lender stays in the foxhole with the builder.

Hear it from Kevan himself — his background in commercial construction, why he builds affordable housing in underserved Houston neighborhoods, and what it took to develop through the pandemic with Tidal Loans behind the project: