American small business is experiencing a strange paradox. According to the Federal Reserve’s Small Business Credit Survey, every third entrepreneur has a credit rating below 640 points. At the same time, demand for startup capital is breaking records – over 5.4 million business loan applications were submitted in 2024 alone. Traditional banks reject 82% of such applicants, but alternative lenders are filling this gap at wildfire speed.

Bad credit history is no longer a sentence. The financing market has changed so dramatically that even entrepreneurs with a 500-550 rating find money for development. New risk assessment technologies, alternative data sources about creditworthiness, competition between online platforms – all this has created an ecosystem where bad credit past has ceased to be an absolute obstacle.

In this article, we’ll look at real financing options for those who can’t boast a perfect FICO score. We’ll talk about five companies that actually work with difficult cases, break down the terms, pitfalls, and how to actually get this money when the traditional banking system isn’t your friend.

How to get a small business loan with bad credit

First, the unpleasant part. If your FICO is below 600, forget about Bank of America or Wells Fargo. They won’t even look. Traditional banks live in a world where credit score is holy scripture, and everything else is details.

But there’s another way. Alternative lenders evaluate more than just your credit history. They look at your bank account turnover, cash receipts, even Google Reviews ratings.

If you’re looking for small business loans for badcredit, the first rule is honesty in your application. Hiding bankruptcy or lawsuits will lead to instant rejection. These companies have access to dozens of databases and check everything in minutes. Better to openly explain why your rating dropped – medical bills, divorce, pandemic – and show how you’re fixing the situation.

Second – documentation. You need bank statements for 3-6 months, tax returns, sometimes a business plan. Even if the lender says “quick approval in 24 hours,” you’re going nowhere without these papers. Prepare everything in advance.

Third – realistic expectations. With a 540 rating, you won’t get $500,000 at 8% annual. More likely it’ll be $25,000-$75,000 at 25-45% annual for 6-18 months. Sounds harsh, but that’s the admission ticket to the game.

Fourth – alternative collateral. No real estate? Use equipment, inventory, even future credit card receivables. Merchant cash advance is a popular option for retail outlets and restaurants.

Top 5 lenders for businesses with bad credit

The market for bad credit small business loans has grown so fast that new platforms now approve applicants traditional banks wouldn’t touch.

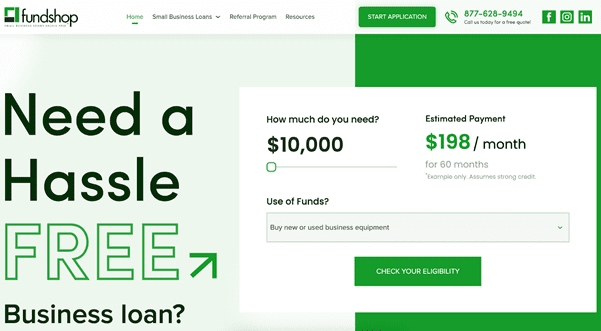

Fundshop

Let’s start with a platform that specializes specifically in difficult cases. Fundshop works with entrepreneurs whose credit rating has dropped to 500 points – a level where most lenders simply hang up the phone.

Their thing is speed and flexibility. You fill out an online form, upload bank statements, and within 48 hours you get a decision. Loan amounts range from $5,000 to $500,000, depending on your monthly turnover. If the business brings in a stable $20,000+ per month, chances of approval are high even with terrible credit history.

Interest rates here aren’t the lowest – from 18% to 42% annual. But the terms are transparent, with no hidden fees for early repayment or “consulting charges.” Fundshop also offers a bad credit business cash advance– an option for those who don’t want fixed monthly payments. You give back a certain percentage of daily sales until you close the debt. In slow months you pay less, in busy ones – more. For seasonal business, this is a lifesaver.

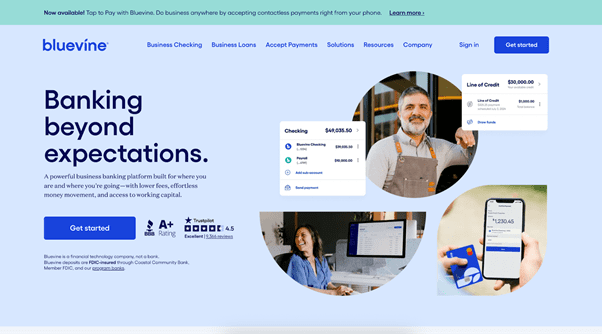

Bluevine

This company made its name on credit lines for small business. Unlike classic term loans, a credit line works like a credit card – you take when needed, pay interest only on the amount used.

Bluevine accepts applicants with a rating from 625, which is still considered subprime. Maximum amount is $250,000, but realistically for beginners with bad credit, $10,000-$40,000 is available. The approval process takes 24-48 hours, money arrives in the account the next business day.

Interesting detail: Bluevine integrates with QuickBooks and automatically analyzes your financial flows. If they see stability and growth, they can increase your limit in a few months without additional applications.

Downside – relatively high cost. Factor rate ranges from 1.15 to 1.45, which translates to an effective rate of 20-35% annual. Plus a mandatory 2.5% fee for opening a credit line.

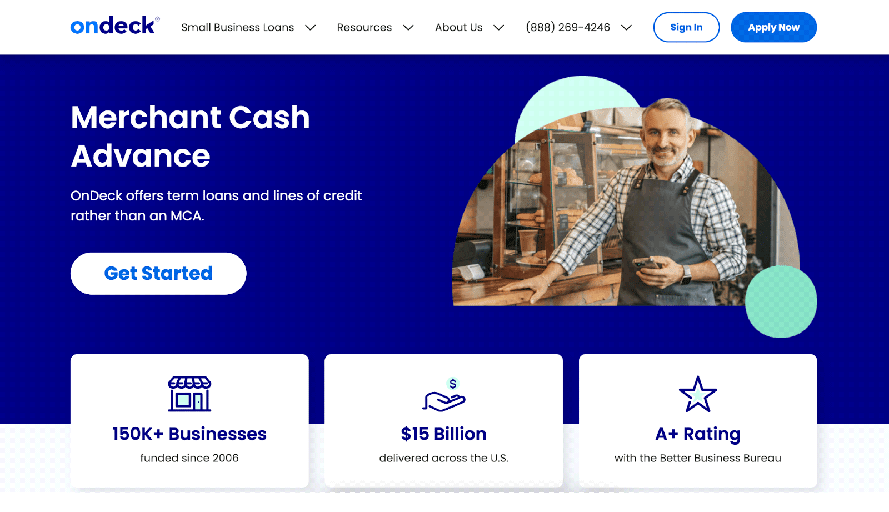

OnDeck

One of the pioneers of online lending, which started operations back in 2007. OnDeck approves borrowers with a minimum rating of 600, but I know cases where they took even 580 if the business had been operating for over two years.

Loan amounts range from $5,000 to $500,000, terms from 3 to 36 months. The key advantage is fixed weekly or daily payments that are automatically debited from your account. Sounds scary, but actually it disciplines you and protects you from the temptation to spend money on something else.

APR (annual percentage rate) starts at 29% and can reach 99% for the riskiest applicants. Yes, almost 100%. But the platform is popular because it works quickly and doesn’t require collateral. According to OnDeck statistics, 70% of their clients use loans for inventory or equipment, not to cover debts.

Important nuance – OnDeck is tough on late payments. One missed payment and interest jumps 5-7%. Two misses – they hand the case to collectors. So take only what you can definitely repay.

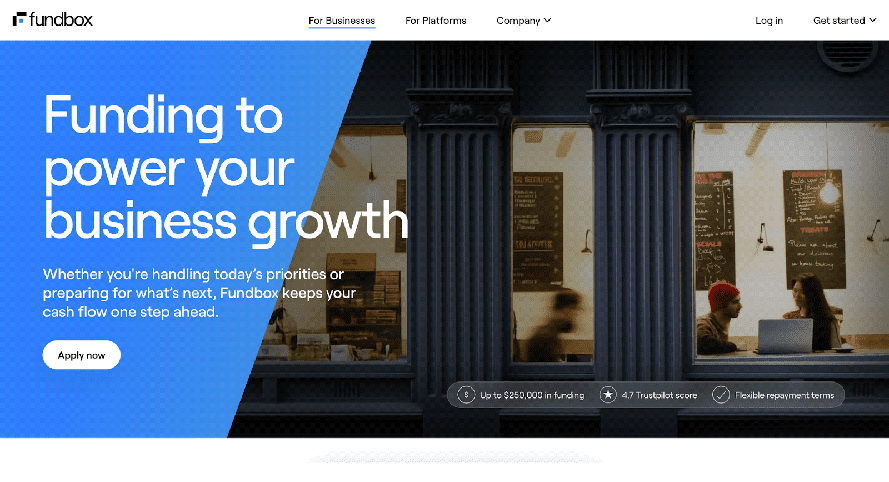

Fundbox

Favorite among micro-businesses and freelancers. Fundbox specializes in small amounts – from $1,000 to $150,000. Minimum credit score is 600, but they really approve even with 580 if they see regular deposits in the account.

The process is maximally automated. You connect your bank account and accounting software (QuickBooks, Xero, FreshBooks), the algorithm analyzes the data and in 5-10 minutes gives a decision. The first loan is usually small – $5,000-$10,000, but after successful repayment, the limit grows.

Interesting pricing model: you pay a fixed weekly fee, not interest. For example, you took $10,000 for 12 weeks – you pay $850 weekly, total you’ll return $10,200. The effective rate comes out to 8-15% for the entire term, which for bad credit is pretty good.

Downside – short terms. Maximum 24 weeks, more often 12. For serious development investments this doesn’t fit, but as a quick cash flow injection – excellent.

Credibly

Last on the list, but not least in importance. Credibly has been operating since 2010 and has established itself as a company for “difficult” cases. They accept applicants with a rating from 500, which is rare in the market.

Specialization – merchant cash advances and short-term loans for retail, restaurants, beauty salons. If your business accepts credit cards and has stable daily turnover, Credibly will consider the application even after bankruptcy.

Amounts range from $5,000 to $400,000, but the average loan for newcomers is $25,000-$50,000. Approval time is 24-72 hours, money in the account in 1-3 business days. Factor rate is high – from 1.20 to 1.60, meaning you return 20-60% more than you took.

What you need to know about small business loans with bad credit

The lending market for problem borrowers is a separate world with its own rules. The main difference from traditional banks is decision speed and cost of money. Where Chase Bank considers an application for a month and then says “no,” alternative platforms say “yes” in a day, but at a premium.

First, forget the term “cheap money.” If you see advertising for “9% loan for any credit rating” – it’s fraud. Real rates for bad credit start at 18% and rarely drop below. Average APR in the alternative lending market is 35-45% annual.

Second, read the terms. Many platforms use factor rate instead of APR, which confuses understanding of real cost. Factor rate 1.30 on $50,000 means returning $65,000. If the term is 12 months, the effective rate is ~30%. If 6 months – already ~60% annual.

Third, early repayment. Some lenders allow closing the loan early without penalties, others take the full amount of interest regardless of term. This is a critically important point that many miss.

Fourth, personal guarantee. Most alternative lenders require a personal guarantee from the business owner. This means that in case of default, they can collect the debt from your personal property. LLC won’t protect you in such a case.

How top merchant cash advance companies evaluate your business

The notion that MCA doesn’t check credit history is a myth. They check, just don’t give it decisive weight.

- The main factor is daily card transaction volume over the last 3-6 months. Most merchant cash advance companies want to see minimum $5,000-$8,000 per month. If your business runs mostly on cash, MCA won’t work. That’s why bodegas, barbershops, and small ethnic restaurants often get rejected.

- Second factor is length of operation. Preferably minimum one year, though some providers approve after six months if sales are stable.

- Third is presence of open bankruptcies or unpaid tax liens. If the IRS has claims against your business, most MCA companies will reject you. Exception: situations where a payment plan has been established with the tax authority.

Interesting detail: NSF (Non-Sufficient Funds) on statements kills your chances faster than bad credit history. If the bank regularly rejects payments due to insufficient account balance, that’s a red flag for underwriters.

- Some advanced companies use machine learning for risk assessment. Kabbage (now part of American Express) analyzes not just bank statements but also social media activity, Yelp reviews, and website traffic. The algorithm can approve those a traditional underwriter would reject.

Conclusions and recommendations

Bad credit business loans aren’t the end of the world, but a tool. Expensive, risky, but functional. Main thing is to understand that you’re buying time and opportunity, not cheap money.Choosing a small business loan with bad credit always comes down to understanding the real cost and having a clear plan for using the capital.

Before submitting an application, do three things.

- First – calculate the real cost of the loan in dollars, not percentages.

- Second – make a monthly cash flow forecast accounting for payments. If even one month goes into the red – don’t take it.

- Third – have a plan B. What will you do if sales drop 30%?

Most important – use the loan to earn, not to survive. Money for salaries or rent is a bad idea. Money for equipment, marketing, inventory for specific orders is a good idea.

And remember that every on-time payment improves your credit history. Alternative lenders report to bureaus, so even a 40% loan can become your ticket to the world of normal financing in a year or two.

The business world is cruel to losers but gives second chances to those willing to pay a premium for their mistakes. Small business loans for bad credit are exactly such a second chance. Expensive, but fair.